Written July 2020, all information accurate at time of writing. As with all investment decisions, your capital is at risk, and remember to complete your own research after reading this introductory guide!

Over the past few years and particularly right now, interest rates on savings accounts are particularly low. While cash ISAs and regular savings accounts offer slightly better rates or reduced tax, if you want higher returns over the long run, investment might be something worth looking into.

Micro-investing is a great way to start getting a feel for investing as you only need to put up a small amount of initial capital, and apps often use AI or questionnaires to auto-build your portfolio. But this method of investing is not the most tax-efficient (if you use a general investment account).

An ISA, or Individual Savings Account is a way for UK residents to save or invest up to £20,000 per tax year each year. You can open one of each of the four different types of ISA each year and split your £20,000 allowance between them (but you’re only allowed to put up to £4000/year in your Lifetime ISA). Currently, you have until the 5th of April 2021 to use this year’s allowance.

The different kinds of ISA:

- Cash ISA

- Innovative Finance ISA

- Lifetime ISA

- You have to be 18+ and under 40

- You can put in a max of £4000 each year until you are 50

- The government will add a 25% bonus to your savings, up to a maximum of £1,000 per year.

- You can hold your funds as cash or invest it as ‘stocks and shares’; after 50 you can no longer pay in nor will you receive the 25% bonus, but the money you can still earn interest or investment returns.

- You can only withdraw your money from the L-ISA if you are:

- Buying your first home (T&Cs apply)

- Aged 60+

- Terminally ill, with less than 12 months to live

- If you withdraw for another reason you will have to pay a withdrawal fee, currently set at 20% but this will go back up to 25% in April 2021.

And the subject of this week’s article…

The Stocks and Shares ISA

What’s the point of opening a Stocks and Shares ISA?

Having a Stocks and Shares ISA, which you can open with some micro-investment apps as well as other providers, you can invest in a wide range of products including company shares, investment funds, corporate bonds and government bonds. Investing through an ISA is more tax-efficient (i.e. if you invest via an ISA you don’t have to pay Capital Gains Tax on your profit, which saves you 10-20% depending on your tax bracket).

Depending on who your provider is, you need around £100-500 to open up a Stocks and Shares ISA. As a student this is a lot of money, and in some cases it may be better to have your money in a Cash ISA or Easy Access Savings account so that you can access it for rent payments and the like. However, spending some time building up a sum of money to invest by putting aside a small percentage of money you may make from jobs, using round-ups on savings apps, or through a stricter budget will be really valuable in the long term.

Investments are long term commitments; while you may not currently be earning huge amounts from your investments, you can drip feed money into the ISA as and when you are able to, and your future profits, for as long as you have that ISA, will always be protected from tax payments.

Note that you want to keep your money invested for at least five years if you can – the longer the better! This is because you have your original investment, the return you make each year on it, and the interest you earn on that return. The power of compound interest means that your money grows at a faster rate over the years, and you earn more the longer your money stays invested. Investing from a younger age means you can take on slightly more risk as you can ride out any troughs in the market and wait for longer term high returns. It’s important to keep in mind the long term nature of investment, particularly at a time like 2020 when the market is, quite frankly, going to shit.

Finally, always keep an eye on the fees! While fund managers or robo-advisors (ready-made portfolios created based on your personal criteria) or tracker funds (products that follow the rises/falls in the stock market) make investing simpler and offer expertise, it’s important to not overpay on provider, manager or platform fees. Shop around if you feel fees are getting too high and you are able to switch to different providers fairly easily.

Shares vs Funds vs Bonds…What does it all mean?

A share is when you buy a piece of a company on the stock market, like Samsung or Sainsbury’s. You then benefit from any dividends (money paid to a company’s shareholders out of its profits) or growth, but the share price could also decline if the company starts to struggle.

Funds can invest in various assets such as shares, bonds, property or commodities; it pools together money from lots of different investors and a fund manager then invests that on your behalf into a diverse array of assets, usually grouped around a particular theme like Emerging Markets or Gold. Funds allow a professional to undertake investment decisions and management, which often justifies the management fee you pay for that service.

Bonds are different, they are a type of fixed income investment. You are essentially lending money to a company or government for a set period of time in return for interest payments. For example, UK government bonds are called Gilts and German federal bonds are called Bunds. You could invest in individual bonds but this is more risky as if you only rely on a single issuer, you are more vulnerable to loss. By this, I mean if a company becomes insolvent or if a political event negatively impacts a government, they may fail to repay your investment. Because of this, many people invest in bond funds that spread your money between a range of different fixed income holdings. Fixed income investments are considered less risky than shares, as income from bonds is paid out before dividends on shares and bond pay-outs take priority over shareholders in insolvency cases.

But how on earth do you pick?

While some providers offer advisory services to help you build your portfolio based on various criteria such as how much risk you’re willing to take, you can also pick your own funds to invest in.

The way I tend to do this is by reading through research undertaken by my provider and others such as Fidelity’s Select 50 or Hargreaves Wealth Shortlist. You can also keep tabs of global and national markets, as well as on various asset types or specific funds by reading the Financial Times or Forbes. It’s important to note that investment means your capital is at risk, and that while you can do research and keep aware of the market, you can never be 100% certain of a positive return on your investment.

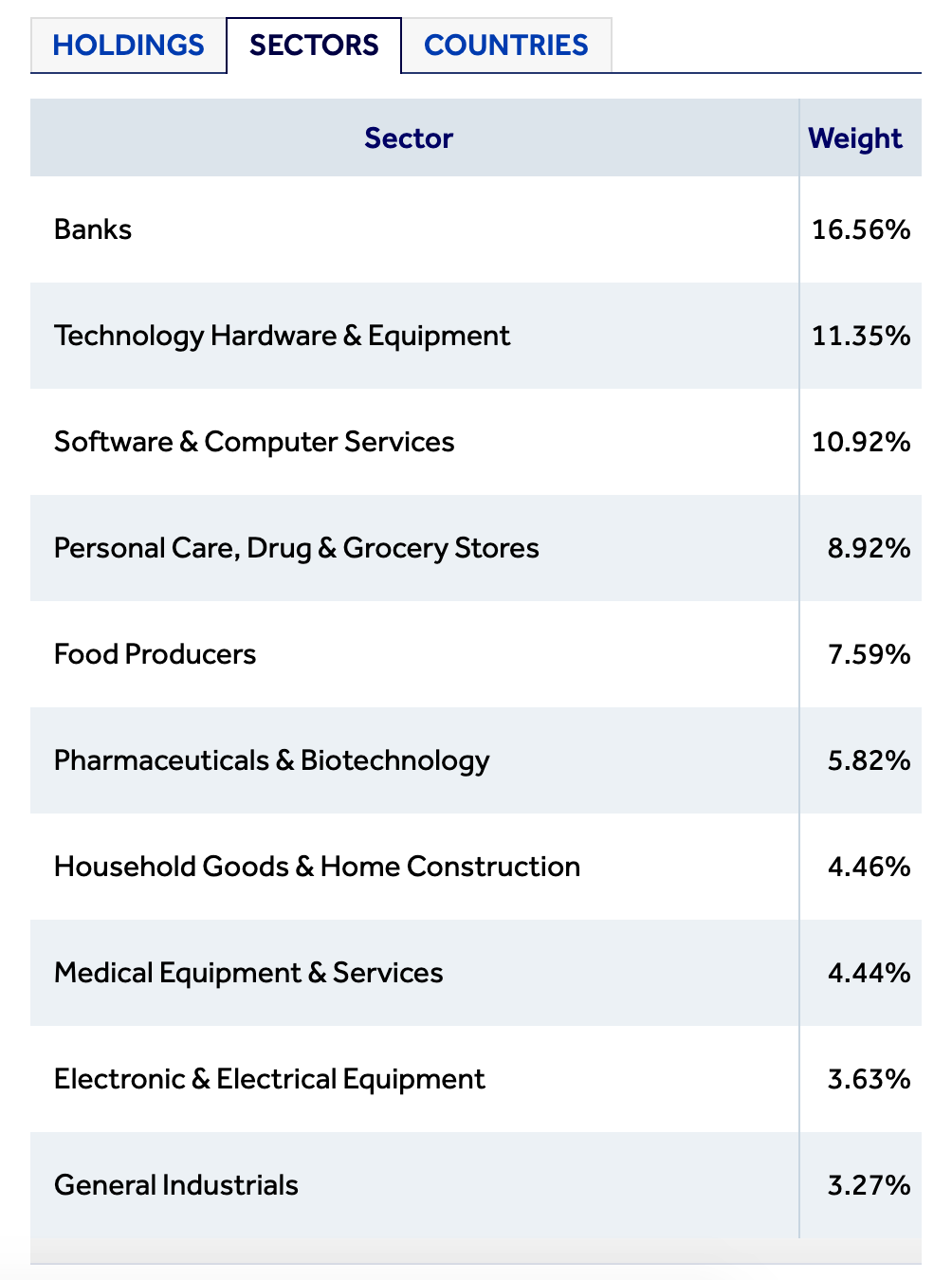

Here’s an example of how I chose a fund that I recently invested in:

Name: First State Asia Focus [Class B – Accumulation (GBP)]

- No initial charge as my platform offset the 4% charge usually levied by the fund management company.

- Net ongoing charge of 0.75% – this is on the high side, but still fits in my personal criteria of keeping this charge at below 1% for the majority of my portfolio.

- I chose the Accumulation fund, which means any income from the fund retained within the fund itself is used to increase the value of the units I hold, rather than the Income fund which distributes any income generated to investors.

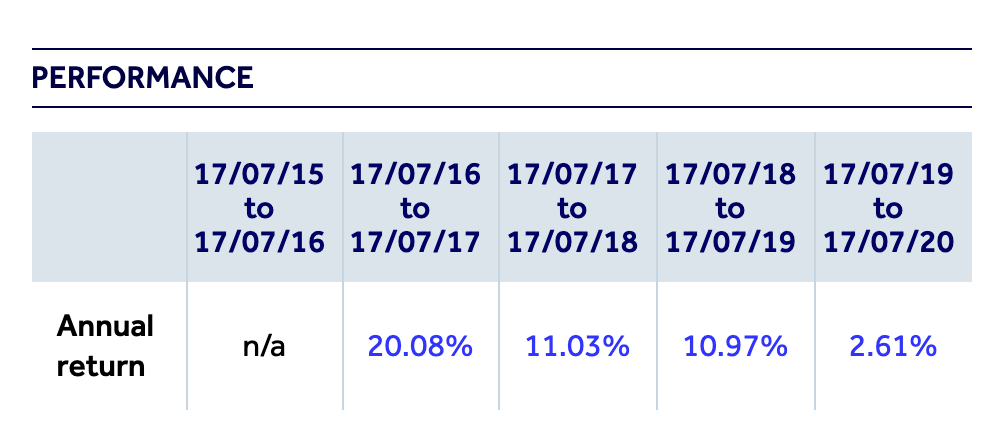

- I then looked at past performance. While it’s relatively new and past performance is not a guide to future returns, it is a good way to see how the fund has done in the past and make a partial judgement about how it may do in the future.

- Here, you can see that the current market has depressed the performance quite a lot between July 2019 and 2020.

- Yet, I made a decision to invest based on how it had previously done quite well; the sector as a whole is one that is generally on the uptick; I have another fund with First State that has done very well; and currently the buying price is very low compared to previous years.

How to open a Stocks and Shares ISA:

While no comparison tool can tell you how a platform or portfolio will perform over time, they can tell you which platforms are right for you based on the amount you have available to invest, cost-efficiency, fee structure and customer experience ratings.

The Times Money Mentor lists the following as top-rated:

- Fidelity Personal Investing Cost Focus Portfolio

- Halifax Portfolio

- Standard Life UK

- Evestor Portfolio

Definitely shop around for the best deal and option for your circumstances – and keep an eye out for changes after you’ve opened an account. I know that I, after doing some more research for this article, am seriously thinking about switching my ISA provider.

As usual, I wish you the best of luck on your personal finance journeys – and please remember I am not an expert, just your friendly neighbourhood money columnist, so definitely complete your own research and make decisions that best fit your own financial situation!