Let’s face it, getting paid never gets old. Whether it’s the rush of your very first pay cheque after weeks of hard work, or a much needed influx of cash just as your budget is starting to wear thin, seeing a positive in your bank statement is a pretty great feeling. However, the actual payslip can be a tad confusing and frankly, to me, looks like something out of the 1970s.

My very first official pay cheque disappointed and mystified me in equal measure because I didn’t realise a chunk of money would be taken out as a National Insurance contribution. More recently, I had to make a (surprisingly quick) call to HMRC to organise a refund on income tax mistakenly taken out of my pay cheque.

So I thought I’d use this week’s column to chat through the basics of interpreting a payslip. I’ll be looking at the tax codes and the purpose of the mysterious National Insurance contribution so that you can cut through the maze of acronyms, shorthand and endless numbers. While error rates in payslips are quite rare, they can still happen – so being able to quickly notice if something is missing or incorrect will save you a headache later on.

The key things to check are:

- Your gross pay i.e. the amount you are paid before any deductions. Do some quick calculations to check you’re being paid your agreed upon rate (if it’s a monthly payslip, multiply by 12).

- Your tax code and therefore amount of income tax paid

- Your national insurance payment

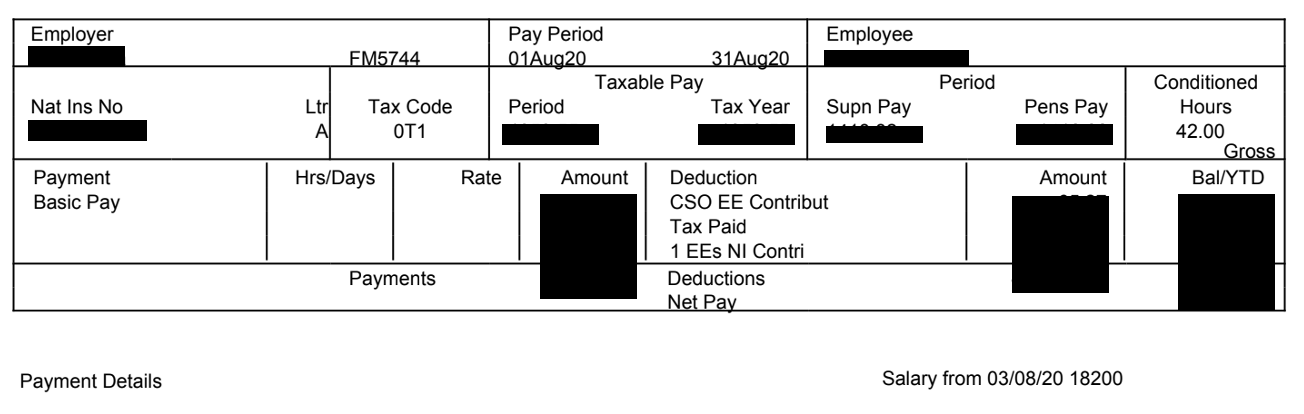

Example of a UK Payslip

- The ‘Supn Pay’ (superannuation pay – your contributions to your company pension plan)

- ‘Pens Pay’ (pensionable pay) are the same, and refer to my gross pay for this pay period.

- The ‘Taxable Pay’ is my pay minus this month’s pension contribution (CSO EE Contribut).

- Bal/YTD is/Year to Date, meaning the total amount I’ve been paid this year.

Tax Codes

Your tax code will normally start with a number and end with a letter, but this is not always the case. Essentially, it relates to the amount of income tax you owe depending on past employment and earning history. Generally, the amount of income tax that you’ll have to pay depends on how much of your total income within the current tax year (6 April 2020 to 5 April 2021) falls within your Personal Allowance, and how much income above this amount falls in each tax band.

Most people are entitled to a standard Personal Allowance of £12,500 this tax year, and any income you earn above this level is taxable. From £12,501 to £50,000, you will pay 20% income tax, and this percentage increases with each further price band.

Since prior to receiving the payslip discussed in this article, I had no formal employment history recorded in the last tax year so I was then automatically assigned the tax code of 0T1. This meant I would have a regular 20% income tax paid out from my earnings. Upon reviewing my payslip, I realised that my earnings in the summer would be within my Personal Allowance. I double-checked what my correct tax code was using the gov.uk tool and then rang HMRC to ask them to alter this on my payslip, as well as to refund the amount via the next month’s payslip.

You can check your Income Tax online to see:

- What your tax code is

- If your tax code has changed

- How your tax code is worked out

- How much tax you’re likely to pay

- You can also let HMRC know about a change that may affect your tax code.

National Insurance

National Insurance contributions count towards certain benefits and pensions such as the Basic State Pension, Maternity Allowance and Bereavement Support Payment. The amount of National Insurance you pay depends on the type of employment you are engaged in, and how much you earn. The rate of payment changes with each tax year, and most people pay the Class 1 National Insurance Rate. For most people in 2020 to 2021, this is 12% of your income if you make between £183-£962 a week, or 2% if you make over £963 a week.

You can see in the payslip the letter ‘A’ next to my national insurance number – this refers to your category (most people are in A). Some others that you might see are X if you don’t have to pay NI, M if you are under 21, H if you are an apprentice under 25, or C if you are an employee over the State Pension age. Rather intriguingly, there seem to be special rules for mariners and deep sea fishermen- so if you end up doing that, perhaps it’s time for a bit of independent research.

Now all these numbers might be starting to give you a headache, but the last thing you might want to check for is any other planned deductions, such as travel stipends, student loan repayments and charitable donations. Finally, do not throw the payslip away (or delete it); keep them in a dedicated folder. While all the information will come to you summed up on the P60 form you automatically receive at the end of the tax year, you might need to use payslips to apply for a mortgage (congrats) or tax credits before this point.