Last week, I wrote about the wonders of the fuck off fund – it’s all well and good saving this pot of money, but the real question is where to store it. The problem is there are so many options to choose from, each with their own weird jargon and pesky set of fine-print T&Cs. So, here’s my breakdown of the various options available for savings accounts and Cash ISAs. I’ll also cover AI budgeting robots who can give you oddly comforting messages like: “you seem to be fucking up less than usual.”

What follows are some key bits of info regarding how to save your money, but as with every financial decision, make sure to shop around and check that the account you choose is best for your situation. Call up the bank or provider to ask all your specific questions, no matter how basic they seem – they’re pretty much always happy to help (unless you get Jim from Accounts who hasn’t had his morning coffee yet).

The basic definition of a savings account is a secure place to put your money and earn interest, so that you get back more than the money you originally deposited (free money, yay!). Here are the four main types of saving accounts:

Easy Access Savings Account

- Interest is paid while the money is in the account, and you can withdraw whenever you want without penalty.

- However, interest rates are usually lower than other kinds of accounts, such as Notice or Regular Savings accounts.

Fixed Rate Bonds

- You set a lump sum of money away for a specific number of years to accrue interest.

- Generally, you are not allowed to access the funds without an interest penalty, nor can you add to the pot.

Notice Accounts

- Unlimited additions, but you can only withdraw money after the stated notice period (which can be from 30 days up to to 6 months).

Regular Savings Account

- These require you to put money away each month with interest paid yearly (unless otherwise stated). They offer higher interest rates than traditional Fixed or Easy Access Savings accounts; but tend to limit the amount of withdrawals you can make, or force you to make a deposit every month.

- The high interest rate usually only lasts for a year, so you might want to ditch and switch after the year is up.

- You could run this account by having an Easy Access Savings account and drip-feeding money monthly into the Regular Savings account.

- You only get interest on your average balance throughout the year. For example, if you reach £4000 by the end, you won’t get interest based on the £4000 but whatever the average was for the 12 months.

- If you’re paying basic-rate tax, you get £1000 of interest tax-free, and if paying high-rate tax, £500.

- Interest rates for ‘open to all’ accounts have dropped in recent years, so they aren’t as lucrative (the best fixed interest ones I could find were Principality BS, Virgin Money and Halifax).

- If you have a First Direct or HSBC current account, or are part of M&S Bank/Club Lloyds, you can get a higher interest rate (2-2.75%). This is a Linked Regular Saver account.

Cash ISAs

If you pay tax on your savings (meaning that you make more than £1000 interest if you are a basic-rate tax payer or more than £500 if you a higher-rate tax payer), you may want to put your money in a Cash ISA.

Cash ISAs are essentially savings accounts that you don’t pay tax on. At the start of the tax year, every UK resident aged 16 and above gets an ISA allowance. For 2020/21 tax year, it’s £20,000. There are different kinds of Cash ISA that have specific rules and interest rates, so make sure you shop around to find the best deal.

- Easy Access Cash ISAs allow you to take the money out when you want, without a penalty.

- Fixed-Rate Cash ISAs often have penalties on withdrawals, or may make you close the account/transfer out to access your funds.

There are many other types of ISA available, for example the Stocks and Shares ISA that I’ll discuss in my piece on investing your money.

‘AI’ Saving?

In recent years, there has been a huge increase in savings and investment apps within the fintech industry. In particular, automatic savings apps which have been designed to analyse your spending, let you input clear savings goals, and then automatically put money away for you. Here are three top rated apps that do this:

Chip

- AI calculates a tailored, affordable amount that will be automatically saved.

- It’s FCA regulated, and is beginning to roll out accounts which you can earn interest on and you can set short/medium/long term savings goals.

- Your money is saved in a Barclays ring-fenced account and is protected up to £85,000 by the FSCS.

- You get charged £1 a month if you automatically (using the AI) save £100+ in 28 days. If you save less than that, it’s free.

However, there have been some negative reviews, stating that some users have had to wait up to two weeks after requesting money withdrawal.

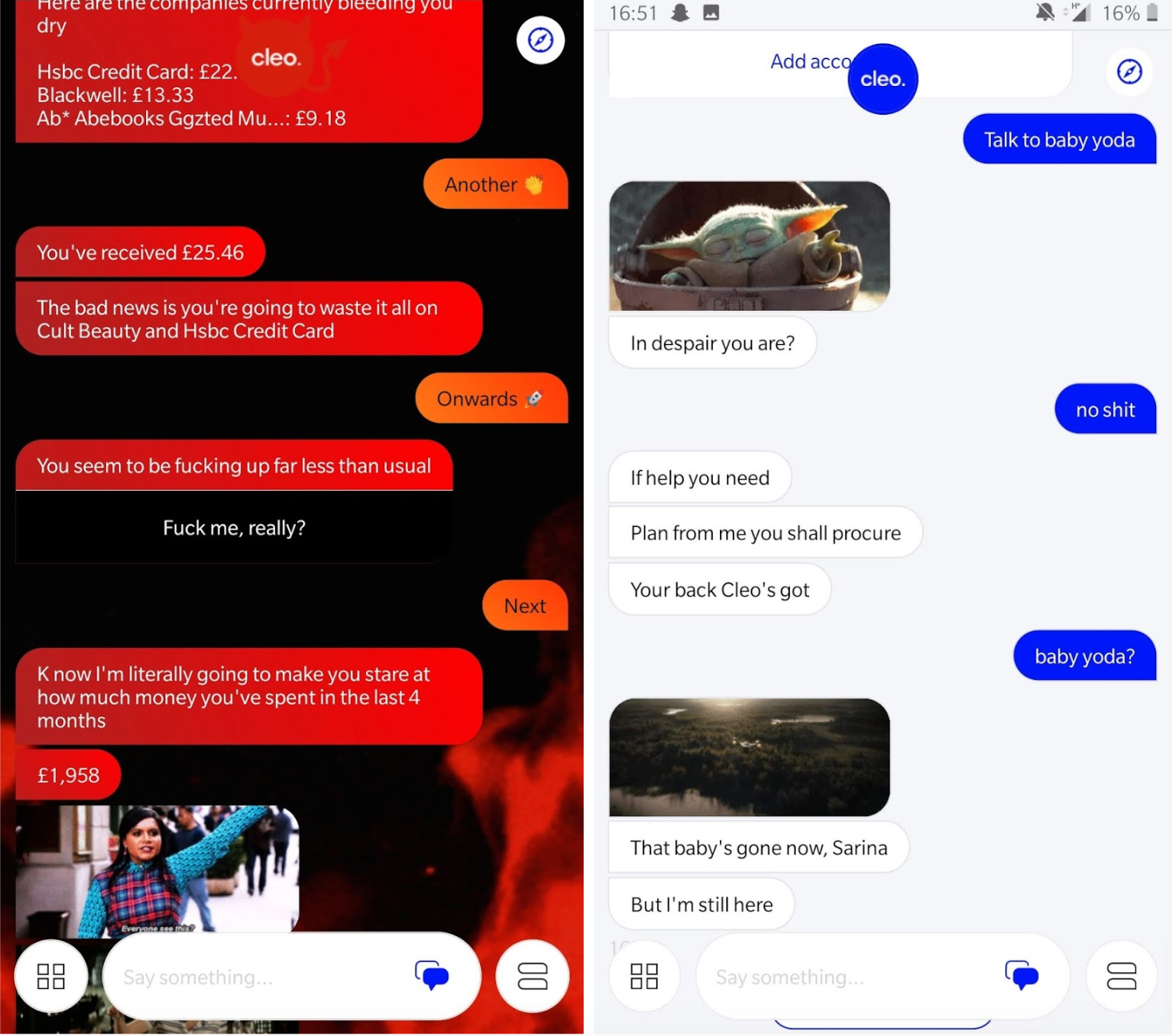

Cleo

- An AI chatbot to help you manage your spending and recommend how much you can afford to save.

- The app will monitor your purchases, notify you when you are close to your limit, and you can set limited period budgets for when you are going abroad.

- Cleo automatically transfers how much it has calculated you can afford to save to your ‘Close wallet.’ You can also move amounts manually and reject suggested transfers.

- The funds, however, are just ring-fenced in an e-money account, and your money does not have FSCS protection. While the app has an £85,000 security pledge, this wouldn’t apply if Cleo itself collapsed – so be aware of this.

Having tried it out myself, the app is great for chatting about your spending without boring a friend and for getting some analytics-backed advice. However, with a lack of FSCS protection, I’m personally unwilling to put my money in a Cleo account, but I have enjoyed the chatbot function a lot.

Plum

- A savings and investment ‘robot’ that analyses spending and automatically saves money based on what the algorithm figures out you can afford.

- There is also an investment feature (more on this in a later piece).

- You can only have one savings pot, unless you pay for the premium version that allows you to create ‘pockets’ for dedicated goals.

Again, be aware that Plum is not covered by the FSCS, although they are authorised by the FCA. They say that as the savings are held as e-money, it is protected by Electronic Money Regulations.

Other fintech mobile banking apps such as Starling Bank and Monzo let you also set up savings pots or goals, both of which are FSCS protected.

Finally, please remember to consult a financial advisor (by calling the bank/account manager) to fully understand all the T&Cs of the specific account you’ve chosen. I hope this helps you navigate the world of savings accounts, best of luck saving!